Other parts of this series:

Carriers looking to start open insurance initiatives must decide which ecosystem best fits their business strategy.

There’s a couple of big decisions that insurers must get right when building an open insurance business. It’s their choice of ecosystem and its supporting strategy.

Digital ecosystems underpin all open insurance businesses. They enable carriers to consume and share data and services with lots of partners. Yet, the structure and composition of such ecosystems can differ a lot. I’ll show some examples later in this post. It’s therefore vital that insurers choose ecosystems that align with their business strategies.

How should insurers choose an open insurance ecosystem?

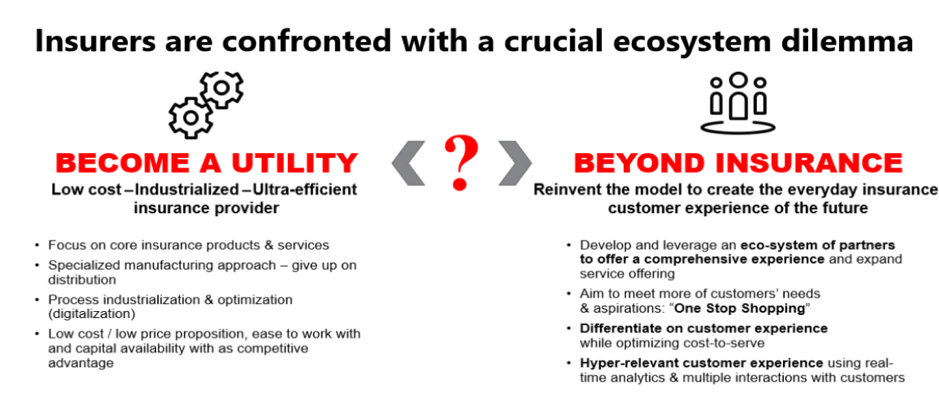

First up, they need to be clear why they’re moving to open insurance. Is it to capitalize on operating and process efficiencies? Do they intend becoming a low-cost service provider for other companies? Or, are they shifting to open insurance so they can transform their businesses? Are they looking to offer an expanded value proposition to their customers which provides them with constant access to a wide suite of services? The illustration below outlines this dilemma. The second route offers the better profit margins. But it requires insurers to venture beyond their traditional markets. They must make much bigger changes to their businesses.

Having navigated through the initial ecosystem dilemma, insurers must then think about the partners they will team up with and how they can jointly add value to their customers. In my experience, this is one of the most challenging parts of the ecosystem journey.

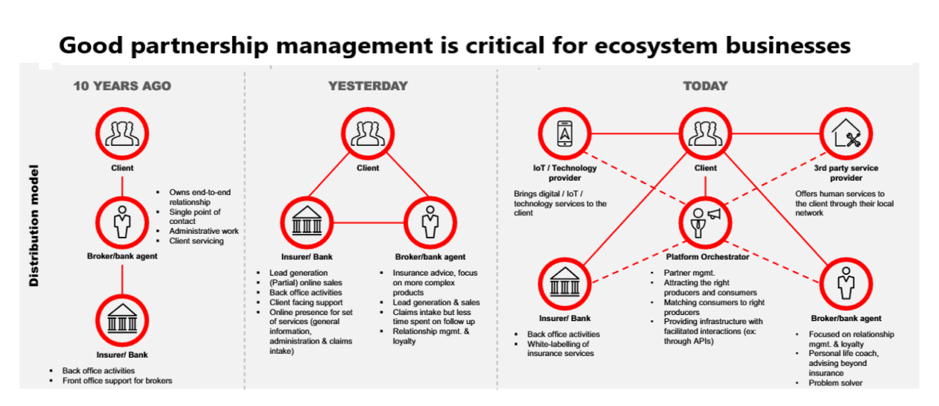

Good partnerships are critical to the success of these businesses. They give insurers access to valuable data and enable them to reach more customers. They can also provide insurers with digital services that complement their own offerings. Carriers have long been aware of the importance of partnerships. With the advent of open insurance such alliances will become critical. Managing these partnerships, as shown below, will be a key priority.

How should insurers develop an ecosystem strategy? When developing their ecosystem strategy, carriers should look first at their current goals. Are there ecosystem opportunities that match their existing objectives? Can they capitalize on these opportunities using their current assets and capabilities? Only then should they should consider opportunities beyond their traditional horizons. Often new and unexpected opportunities can arise out of ecosystem partnerships. Many of these opportunities will be outside the traditional insurance industry.

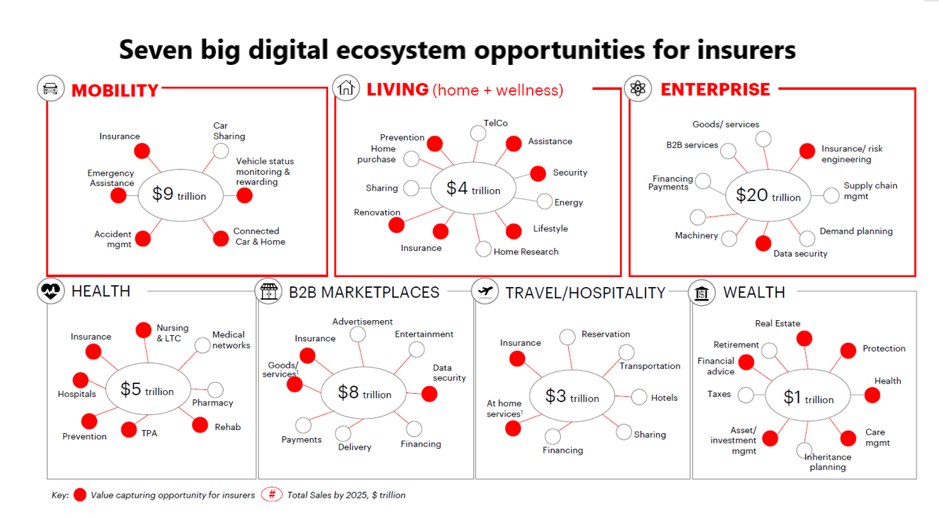

We’ve identified seven big ecosystem opportunities for insurers. I’ve illustrated them below. The combined value of these ecosystems could reach as much as US$50 trillion by 2025.

All these ecosystems generate value for insurers, their partners and their customers. They do this in four ways:

- They give customers an easy “frictionless” gateway to a host of digital services.

- They harness the “network effect” of platform businesses. They offer participants in the ecosystem more value as data traffic increases.

- They thrive on the flow of big volumes of data between large numbers of participants.

- They operate across one or many technology platforms. Each of these platforms is managed by a trusted service provider.

Insurers need to choose their role in the ecosystem economy.

Having settled on the right ecosystem for their open insurance business, carriers face another big decision. What ecosystem role should an insurer perform? Let’s have a look at the main options:

Ecosystem initiator. Insurers such as Ping An have built their own big ecosystems. They generate huge volumes of data traffic and deliver a vast array of products and services. The Ping An ecosystem hosts offerings from many of the group’s diverse subsidiaries. It also offers services from a long list of third parties.

Ecosystem orchestrator and value architect. Several insurers have built strong ecosystem businesses that include offerings from business partners. USAA and Discovery, for example, have taken this route. They’ve upped the value of their ecosystems by pulling in services from partners.

Ecosystem player. Insurers can build strong businesses by using other companies’ ecosystems. Both Zurich and Groupama have done this. They’ve positioned themselves as key components of established ecosystems. They’ve tailored their insurance services to suit these specific channels.

Plug-and-Play insurer. Firms such as La Parisienne have chosen an insurance as a service (IPaaS) approach. They deliver specialised insurance services across an ecosystem. IPaaS offerings may include ecommerce, payments and analytics services.

As I mentioned at the beginning of this blog post, insurers have many different types of ecosystems they can choose. They also have a variety of roles they can perform. Making the right choices, early on the ecosystem journey, will go a long way to ensuring success.

For more information about open insurance or ecosystem businesses look at the links below. Otherwise, send me an email. I’d like to hear from you.

Open Insurance: Unlocking Ecosystem Opportunities for Tomorrow’s Insurance Industry.