The COVID-19 pandemic continues to cause upheaval in our business and personal lives in North America and around the world. While there is still considerable uncertainty around how the pandemic will continue to evolve, insurers need to continue to look forward and plan for the future. They’ll want to consider the outlook for the industry over the next five years and determine if their current revenue strategies are aligned with the coming opportunities.

Insurance industry premiums are expected to grow over the next four years

Accenture research suggests that the insurance industry is expected to grow from $6.1 trillion in gross written premium (GWP) at the start of 2020 to $7.5 trillion by the end of 2025. This includes $800 billion in US healthcare payer premiums. While managed healthcare plans haven’t traditionally been counted as part of the insurance sector, they’re now considered material due to blurring boundaries between digital health products and services.

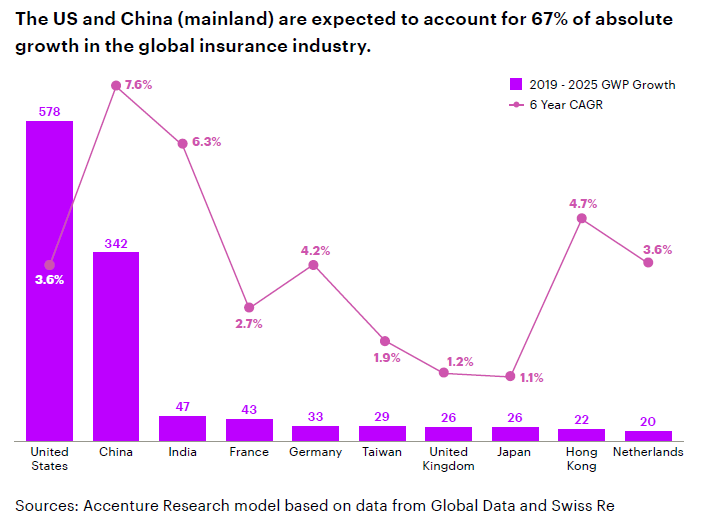

While emerging markets in Asia Pacific—most notably China (mainland)—are driving up the global average, the US is set to take up a huge proportion of absolute growth. In fact, between them, the US and China are expected to account for more than two-thirds (67%) of growth.

Why is innovation an important part of this outlook?

Of that $7.5 trillion in GWP, almost half a trillion dollars ($480 billion or 7%) is likely to be heavily impacted by innovation. We anticipate seeing GWP affected by new risks, product offerings and services, product innovation and shifting placement channels. With hundreds of billions of dollars at stake, North American insurers need to identify which innovations offer the greatest opportunities for revenue growth—and take maximum advantage of them.

Four areas of innovation offer the most potential for revenue growth

When I talk with our insurance clients, I recommend four areas of innovation that I think will be particularly advantageous in the next five years and beyond.

1. Health/wellness and life products and services. With a revenue opportunity for insurers worth $120 billion, innovations that focus on smart health products, products and services for aging populations, and direct life and wealth management products are worth considering.

By 2030, 20% of US citizens will be 65 or older. Add to that the increase in average life expectancy, which now stands at almost 79 years, and the US is on track to see a surge in demand for healthcare and escalating costs. But smart health products, such as those that enable remote patient monitoring, will let people stay in their homes longer and should lessen their need for expensive care. Of course, wearable technology isn’t just for the aging population. Trends suggest that devices that help us monitor our health and keep us safe will remain a priority.

Beyond preventative measures, the aging population also needs innovative insurance products that address their care management and financial security concerns. The 2019 Secure Act aims to extend retirement savings opportunities and expand access to annuities in 401(k) plans. So, this is another key area of interest for insurers.

2. Sharing economy, climate change and cyber threats. These three risks present potential insurance revenue reaching $115 billion. For instance, in the sharing economy, people are opting out of asset ownership, which means reduced premiums for fewer assets. However, in place of this, leading insurers are tapping into the market with offerings that fit with newly formalized sharing arrangements.

One example of this is insurance for short-term rentals. Through Airbnb and other similar services, people rent out one or more rooms, or their entire home, to vacationers. To mitigate against the risk of doing this, rental property owners purchase insurance. Coverage might include replacement costs for the property and contents, damage caused by a guest and loss of rental income if there’s an insured property loss.

When it comes to climate change, we’ve all seen the increase in catastrophic storms and wildfires. According to the National Centers for Environmental Information, 2020 set a new annual record with 22 severe weather events in the US—and that counts all the wildfires as a single event. Furthermore, 2020 was the sixth consecutive year with 10, or more, billion-dollar weather and climate disaster events. There’s potential here for insurers to collaborate with reinsurers to cover new and evolving risks associated with the climate.

Cyber threats also offer insurers new opportunities, not just in terms of cyber insurance, but also around pre- and post-incident advisory servicing. I see this as an area where the massive disruption in the value chain will continue, with insurers, reinsurers and brokers delving heavily into advisory and risk management solutions. Read about what types of cyber threats are expected here.

3. Technology integration within traditional products. As technology is increasingly integrated with traditional products, insurers can expect revenue opportunities worth $120 billion. In this area, I recommend insurers focus on smart auto, smart home and smart manufacturing and building.

In-line water shutoff devices are just one example of a smart device that can save homeowners and insurers money by reducing the severity of damage from water leaks. Also, as my Accenture colleague Markus Hayek said recently, smart sensors integrated into a manufacturing production line and real-time analytics could save companies (and their insurers) millions of dollars.

With access to more data from connected devices, insurers will be able to further customize the coverage they offer based on actual risk. But to really take advantage of this innovation, insurers need to be sure that they have the right data, that they’re leveraging relevant external data sets and that their data is cleansed and harmonized. Quality of data is critical. Plus, they need a robust analytics capability to glean insights from the data. This is one area where I believe insurers shouldn’t skimp if they want to seize opportunities for growth.

4. Shift to alternative distribution. This final area of innovation could see revenue opportunities worth $125 billion in shifting premiums. New entrants to the market, including non-insurance companies like Tesla, are beginning to offer insurance products and insert themselves into the insurance value chain.

There’s an opportunity here for insurers to show themselves to be easy ecosystem partners. By doing this, and by offering usage- (servitization) and behavior-based offers, they’re more likely to retain existing customers and attract new ones. They also have an avenue to additional sales opportunities, vehicle-to-home integrations and data monetization.

Technology Vision for Insurance 2021: We outline five emerging technology trends that will impact the insurance industry in 2021 and beyond.

LEARN MOREWhere should insurers start?

For insurers wondering which of these areas of innovation to address first, I suggest starting in areas you’ve already focused some effort. It’s easiest to build on the momentum of existing initiatives, and then branch into new areas. Remember too, that your geographic location makes a difference. Not every global trend will be applicable in your market and regulatory requirements vary significantly. This might make some opportunities a higher priority for your business.

If you’d like to talk through your own scenario and explore how you can take advantage of any of these opportunities, please feel free to reach out to me directly. We have a Strategic Resilience modeling tool, designed specifically for insurers, that can help you pressure test and refine strategic investments and measure total opportunity.

Or, if you’d like to learn more about where we see the insurance revenue landscape headed, read the report: Insurance Revenue Landscape 2025: Innovate for Resilience