Other parts of this series:

What does the phrase “strategic resilience” bring to mind? It probably makes you think about being prepared for the future. But how do you prepare for an unpredictable future, including rapidly evolving technological innovations, constantly evolving customer and employee preferences, expanding environmental challenges and increasing complexity of government regulations, just to name a few? And what do you do when the future you thought would happen, doesn’t? Or when the future you thought would happen in ten years actually happens in five? Is it possible to prepare for multiple futures?

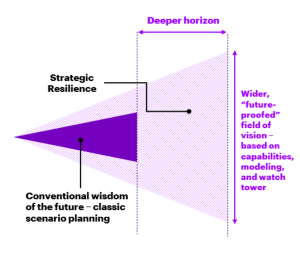

In this blog series, I will explore these questions using Accenture’s strategic resilience framework and modelling to show how scenario planning for the future shouldn’t be a guessing game—and it doesn’t need to be a purely academic exercise, either. You can, and should, harness the power of information we have today to build flexibility and durability into your business model to thrive now and be prepared for tomorrow.

The future for insurance is filled with uncertainty

It turns out, the future is hard to predict. We get a lot of things wrong, from election results (Brexit) to technology trends (how many autonomous vehicles are roaming your neighborhood?) and a pandemic that was a shock to the globe.

When you look at the insurance industry specifically, there are many developments that are hard to predict. Three of the biggest are: emerging risks (aging population, climate change and cyber attacks), the sharing economy (freelancer, auto, home) and the smart economy (technology-integrated products). The specific questions within these areas highlight just how unpredictable the future is:

- What will the lasting impact from the COVID-driven recession look like to the insurance industry (e.g., shifting demand)?

- How are emerging risks going to affect the industry in the short-, medium- and long term?

- How will consumer preferences and the sharing economy impact insurance product manufacturing and distribution?

- How will increasing environmental catastrophe risk impact (re)insurance markets and demand?

- How will the scope of business liability be expanded or contracted?

- To what extent will adoption of advanced technologies (e.g., AI/ML/VR) disrupt insurance processes?

Given that there is so much unknown, are we left to guess about how these will play out in the future—or worse, simply wait and see? The answer is no.

Accenture’s framework for strategic resilience

While predicting the future isn’t possible, we can identify triggers that lead to market shifts. We can also use historical data and industry insights to model current trends (using a model we’ve developed for this purpose) to outline different future scenarios. These scenarios represent how key trends might lead to different outcomes under different circumstances. Based on this information, we can determine which strategies would be most appropriate based on considerations such as financial opportunity or risk.

We begin by outlining current and future trends using the PESTEL framework: political, economic, social, technological, environmental and legal. From there, we determine where each trend is currently headed—the baseline. The next step is the crucial part of strategic resilience modeling: What happens if a trend changes course due to an unforeseen event or shift in the market?

This is where scenario planning comes in. We outline different scenarios based on potential changes to each trend. But our strategic resilience framework is more than just a scenario modeling exercise. We can use real-world data and financials to see where the most opportunities and highest risks are within each future scenario. Armed with that knowledge, we can determine the most appropriate long-term strategies for a particular business.

Let’s look at a quick example. Historically, small commercial insurance has been an underserved market with low premium revenue and high support needs to acquire and provide necessary coverage. Websites like Etsy, eBay and Amazon make it easier than ever to sell products, while apps like Uber and DoorDash have established a gig economy. A whole generation of new business owners has been created. These business owners and their workers need insurance, but most will still represent very low premiums on an individual basis.

This group has also expressed digitally savvy preferences for shopping and servicing. If companies missed these burgeoning new business owners and underappreciated the multi-year trends of data proliferation, combining digital capabilities and the consumerization of B2B, then they are likely just now realizing that there is a growing and accessible market (albeit still in development).

Insurers are responding as they see digital InsurTechs such as NEXT and Vouch build new business models and steal market share. Legacy players are entering or expanding their digital presence in the small business market, such as Berkshire’s biBERK and THREE insurance. USAA recently launched a small commercial model to support the needs of business owners in the veteran community. New distribution ecosystems are also emerging via the brokerage market to provide small commercial coverage through a digital model, such as Aon’s CoverWallet.

Instead of reacting, Accenture’s strategic resilience framework could have shown this potential opportunity before it was apparent. By outlining multiple potential scenarios and then analyzing financial opportunity and risk for each, insurers would be able to look at the implications of different potential futures and make a well-informed, data-driven decision.

The specific decision will depend on a business’s current realities, needs and long-term goals. The point is to systemically analyze current trends, build-out flexible scenarios based on potential changes and then make informed decisions that are specifically designed to build resilience in the business.

The markets, product lines, channels, value propositions and technology you choose to invest in—these choices all influence a company’s strategic resilience.

In the next part of this series, I will narrow my focus to a major category impacting the world: sustainability and ESG (environmental, social and governance). I will explore the key ESG trends that are currently impacting the insurance industry and go through specific scenario planning to illustrate the power of strategic resilience.

In the meantime, if you are looking to build a long-term strategic roadmap that is resilient and takes future unknowns into account, then please reach out to me here.