Other parts of this series:

Can new and emerging technologies reignite a dying life insurance industry?

In Europe, life insurance is a dying business. People just don’t buy it anymore. Next-generation customers—Millennials and Generation Z—simply don’t see the relevance or value of good, old-fashioned life insurance. The decline doesn’t end in Europe: life insurance in China has lost its appeal and in the US, only 44 percent of households have individual life insurance.

Yet there are a few outliers—for example, John Hancock in partnership with Vitality—that have created life insurance offerings that appeal to young and old. In my previous blog series, I asked: What is keeping insurers from reaching their true potential? In this series, I will explore how insurers can use technology to create new business opportunities. But first, they need to embrace the new normal.

Technology is the fabric of reality

We are living in a new post-digital world where technology is the fabric of reality. According to the newly released Accenture Technology Vision for Insurance 2019 survey of thousands of business and IT executives, including 577 in insurance, 96 percent of the insurance executives reported that the pace of innovation in their organizations has accelerated over the past three years owing to emerging technologies.

It started with digital-born companies like Google, Amazon, Facebook and Apple showering consumers with digital products and services. Today, digital-era technology is no longer a differentiator; it’s expected of every business, including insurance companies.

Insurers are facing a higher level of expectations from their digitally mature customers, employees and business partners than ever before—and to meet these expectations, they need a more holistic understanding of the people, assets and businesses they insure. They also need to understand that their outlooks and needs are changing continually.

How can insurers meet these ever-changing expectations?

In the post-digital world, every moment will represent a potential new market of one. Consumers can communicate their demands immediately and expect it to be met instantly. With technology, insurers can meet people’s needs anytime, anywhere and instantly—if they rise to the challenge.

It’s no longer a question of ‘keeping up with the digitals’ and insurtechs. Insurance organizations that want to digitize their core business must set the following new goals:

- Move your focus to the end. As insurance companies begin to understand instant demand and supply options, they will have more opportunities than they can pursue. Success will mean carefully choosing the specific opportunities companies want to target—and just as important, the ones not to target—then working backward to determine how they will get there.

- Define what it means for your business to be post-digital as the world moves into a new phase of cooperation. As insurance companies settle on their new goals, and the pathways they will take to reach them, they must also determine which ecosystem partners they need and where their own place in the ecosystem should be.

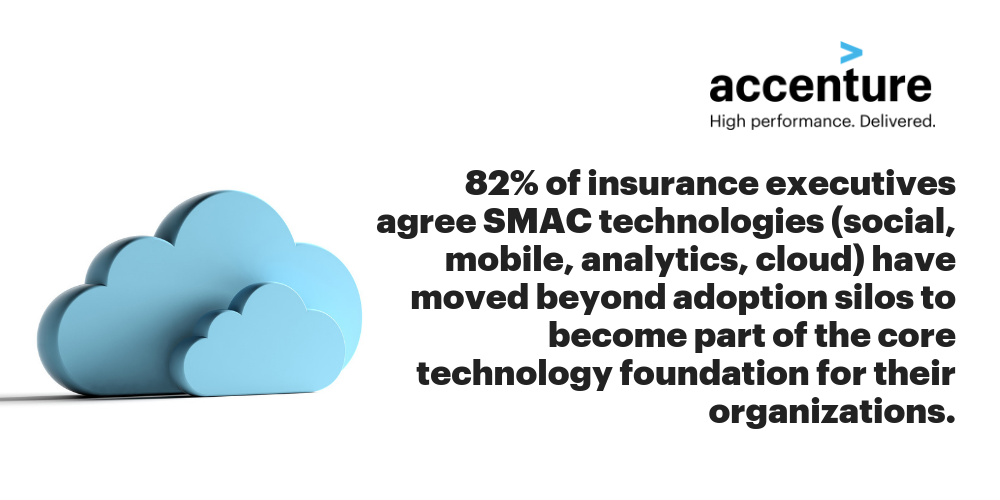

- Master technology innovation as a core competency and a foundation to rotate to what’s next. Failure to hone their expertise in social, mobile, analytics, and cloud (SMAC) will leave businesses unable to serve even the most basic demands of a post-digital world. Mastering SMAC will position insurance companies to catch the next wave of technology disruption—Distributed ledger technology, Artificial intelligence (AI), extended Reality, and Quantum computing (DARQ).

The new normal: hyper-personalized, on-demand digital services

We’re already seeing leading examples of insurance organizations that are figuring out how to shape the world around people and pick the right moments to offer their products and services. Soon, each individual will have their own reality, and every moment will represent an opportunity for insurance companies to play a role in shaping it.

North American life insurer John Hancock has integrated the Vitality behavioral change program into all of its life insurance. It offers policies that track customers’ fitness and health data through wearable devices, allowing them to earn rewards, discounts and gift cards for reaching their exercise goals, logging workouts and buying healthy food. The results are impressive:

- Policyholders on Vitality engage with John Hancock nearly 600 times a year. (The average traditional insurance customer engages with their life insurance company once or twice a year.)

- This intense engagement builds customer loyalty and satisfaction.

- Vitality customers incur 30 percent lower hospitalization costs on average than the rest of the insured population.

The post-digital era is upon us and with it comes a wealth of new opportunities for insurers. Are you ready for what’s next in insurance? Take a look at the Accenture Technology Vision for Insurance 2019 for more insight, or get in touch with me here.