Other parts of this series:

Digital insight into customers can help insurers deliver rich, individualized, experience-based relationships in the post-digital age.

In this series so far, I’ve looked at technology as a catalyst for transformation in the insurance industry and explored how new and emerging DARQ technologies can create new business opportunities.

In this post, I’ll dive into the second trend highlighted in the Accenture Technology Vision for Insurance 2019: Get to know me. This shows how digital demographics are becoming a more powerful way to get to know your customers as individuals.

For me, this trend is particularly relevant to the point I raised in my first post on how life insurance is dying in Europe and further afield. Perhaps it is what’s needed to revive the struggling industry—it is, after all, the individual that sits at the heart of life cover. Here’s how you can use technology to really get to know each customer at an individual level.

Technology identity: get to know your customers

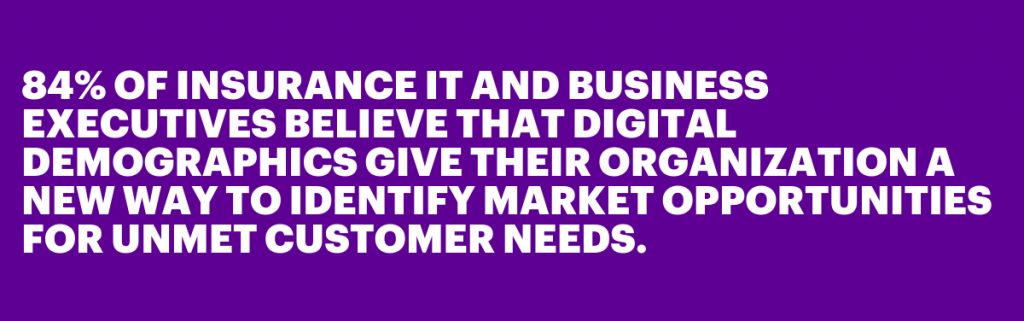

In our research on the trends that will reshape the insurance industry over the next three years, we found that our everyday technology-driven interactions are creating an expanding technology identity for every consumer.

Think about it: everyone you know, with a few exceptions, leaves an online trail of their everyday digital interactions. They connect with people on social media, buy their groceries online, leave queries (more often complaints) on websites, buy books, games, and electronics from Amazon, review and engage with products on digital forums, and search for everything they want to know on Google. Not to mention the dozens of apps with which they engage each day.

And digital demographics are not just about the online world anymore. Today, an array of sensors, wearables, telematics devices and Internet of Things (IoT) technologies provide insurance businesses with a wealth of data about the offline behavior of consumers and commercial customers. That gives insurers the ability to unlock richer insight into the daily risks, needs and behavior of consumers and businesses.

But with richer insight comes greater responsibility for insurers. As they use technologies to embed their services more deeply into the lives, assets and businesses they insure, they must address the privacy, safety, ethics, and governance questions that come along with that level of access.

More than 80% of financial services consumers are willing to share more personal information with their bank or insurer in return for benefits such as lower pricing, priority service, or more personalized service.

With such a wealth of personal data at their fingertips, insurers walk a fine line between tailoring their offerings to a specific customer’s life and losing the customer’s trust. Just because you can use customer data, doesn’t always mean you should. Too many businesses today irritate their customers by bombarding them with experiences that are out of sync with their needs and expectations—or worse, violate their trust. Leading insurers are looking at how they can get the right balance.

This living foundation of knowledge will help insurers not only to understand the next generation of consumers, but also to deliver rich, individualized, experience-based relationships in the post-digital age.

In a post-digital world, we find ourselves engaging in a technology-driven feedback loop. As insurance companies use digital demographics to get to know their customers, they can build new products, services and experiences—and this shifts the transactional exchange of premiums and claims to a richer, ongoing, customized relationship. Forward-looking insurers are using technology identities to personalize their existing products and services, while leaders can push further to craft experiential business models entirely around the technology identities of their customers. These insurers are rising to meet the demands of their customers.

Accenture’s 2019 Global Financial Services Survey of 47 000 consumers found that:

- Two-thirds are confident users of new tech and online services.

- 31 percent would like their bank or insurer to offer new channels such as wearable devices or bots.

- 44 percent would be willing to buy insurance from an online service provider such as Amazon or Google.

The value of knowing your customer

The South African multiline insurer Discovery—through its behavioral change program Vitality—is one of the outliers I spoke about in my first post that are making insurance appealing to young adults.

Through its Smart Life Plan, policyholders under 30 get up to 100 percent of their premiums back for driving safely—tracked through a telematics device—and for living a healthy and active lifestyle—monitored by the Vitality Active Rewards program. This approach has vastly reduced mortality and morbidity risks among young insurance customers by encouraging and incentivizing positive health and driving habits. Once they turn 30, the plan converts to a Classic Life Plan. This way, the insurer encourages people to get life insurance when they’re still young.

Discovery’s Young Adult benefit is a hybrid pay-as-you-drive and traditional comprehensive motor insurance product for drivers under 26 years old. The driver receives comprehensive daytime driving cover as well as 24-hour cover for non-accident perils. Those who drive at night—which is far riskier—are charged an additional per-kilometer premium for trips taken between 9:30 pm and 5:00 am.

SCOR Global Life has partnered with Garmin Health and uses data from Garmin wearables to incentivize healthy living in the Asia-Pacific region. It also assesses an individual’s biological age—and if it’s lower than their chronological age they receive rewards like discounts and health and wellness coaching.

More than 80% of financial services consumers are willing to share more personal information with their bank or insurer in return for benefits such as lower pricing, priority service, or more personalized services.

Insurers that wish to get to know their customers through digital demographics must ask the following questions:

- How is technology an inextricable component of my customers’ identities?

- Are we using customer technology histories to build and evolve our understanding of individual customers?

- How is our business determining the limits of personalization?

- How do I use technology to meet my customers’ rising expectations without violating their privacy and trust?

In my next post, I’ll explore how insurers can meet their customers’ demands as they arise. Until then, have a look at the Accenture Technology Vision for Insurance 2019, or get in touch with me here.