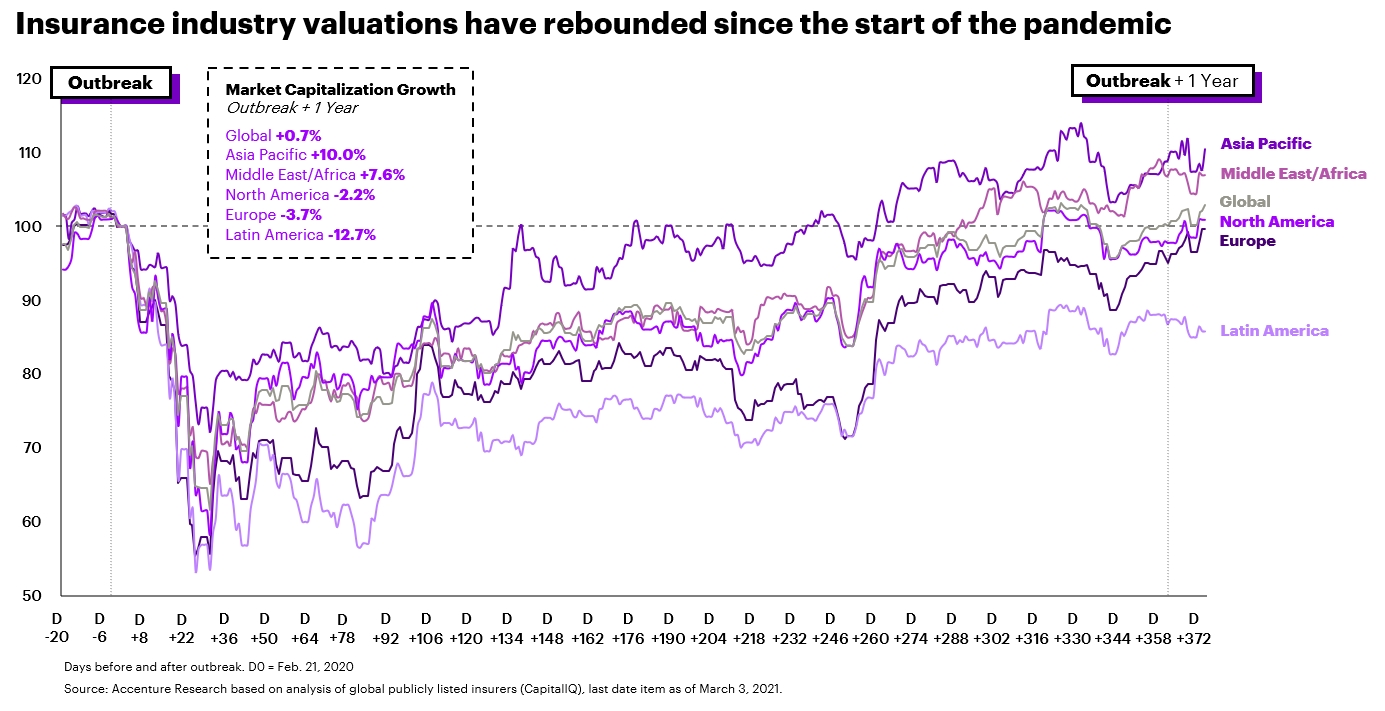

The insurance industry has proven its resilience. Through the disruptions of COVID-19 and massive claims from storms and other catastrophic events, valuations have gradually improved.

Despite uncertain and extreme conditions, forecasts for increased global GDP now signal greater demand for Insurance coverage. In our latest report, Insurance Revenue Landscape 2025: Innovate for Resilience, my colleague Ravi Malhotra and I describe what we see on the horizon.

Our revenue model considered: changing customer demands, how insurers are responding from the supply side, impacts of 70+ trends, and the dynamics of global revenue pools. Based on these analyses, we expect insurance industry revenues to grow by $1.4 trillion to $7.5 trillion over the next five years.

This includes a U.S.-centric $800 billion in healthcare payer premiums. While managed healthcare plans have not traditionally been counted as part of the insurance sector, they are material in this context. Global demand for wellness offerings, including digital health products and services, are blurring traditional industry boundaries.

While we expect an overall six-year compound annual growth rate of 3.5 percent, we don’t expect this growth to be evenly distributed. Emerging markets in Asia Pacific are driving up the global average. This is most notable in China’s outsized GDP growth.

It’s no “rising tide”

Staying the course really isn’t an option this time. Almost half a trillion dollars ($480 billion, approximately 7 percent) of the $7.5 trillion in gross written premium expected in five years, will be heavily impacted by innovation. We anticipate $200 billion from new risks, $140 billion in existing revenues impacted by product innovation, and $140 billion in shifting placement channels.

With innovation-led revenues poised to replace traditional revenues in many product lines, insurers will have to innovate for both retention and growth. Meanwhile, they will need to make scenario-based plans that help build resilience into their strategies.

Profitability is increasingly constrained

Even the most innovative insurers will recognize the harsh realities of industry profitability. Improved pricing in a hardening market will be counter-balanced by elevated exposures from emerging risks and with increasing competition from new market entrants. Investment income also remains stubbornly low with non-life and life insurers seeing book yields averaging 3 percent and 4 percent respectively.

As a result, we expect combined ratios to fluctuate around 100 percent leaving underwriting profitability flat. Average expense ratios are also likely to remain in the high 20s, as average attritional loss ratios climb marginally from their current level in the low 70s (source: Property-Casualty Forecast and Analysis – 20Q4, Conning).

Concerns over increasing catastrophic risk and increases in systemic risks, such as climate change, cyber threats, and business interruption, call for more sophisticated risk models and the regulation of loss aggregation. The projected modest single-digit surplus growth will need to be supplemented with increases to capital reserves (or a reduction of exposure), further reducing the return on equity.

In the face of changing consumer habits, and the changing nature of risk, our new report looks at how insurers can innovate for growth and retention over the next 5 years.

Learn moreReimagining insurance, both externally and internally

To succeed, insurers need to reimagine customer engagement, create a differentiated set of products and services, and invest in future-ready business capabilities to support them. Insurers need to build offerings that provide risk mitigation and ongoing monitoring to manage and protect against risk. Delivering these reimagined offers requires real-time gathering and monitoring of sensor data and enhanced data and analytics capabilities to predict and act on gathered data.

Future-ready insurers will have transformed the value they offer through intelligent, digitally enabled operations and processes at every touchpoint. Insurers who take a future-ready approach will rethink how work gets done across dimensions of technology, processes, and people.

To learn more about what actions to take to seize new revenue opportunities and retain customers seeking innovative digital offerings, read our report: Insurance Revenue Landscape 2025: Innovate for Resilience.