Generative AI (GenAI) has the potential to transform the insurance industry by providing underwriters with valuable insights in the areas of 1) risk controls, 2) building & location details and 3) insured operations. This technology can help underwriters identify more value in the submission process and make better quality, more profitable underwriting decisions. Increased rating accuracy from CAT modeling means better, more accurate pricing and reduced premium leakage. In this post, we will explore the opportunity areas, GenAI capability, and potential impact of using GenAI in the insurance industry.

1) Risk control insights zone in on material data

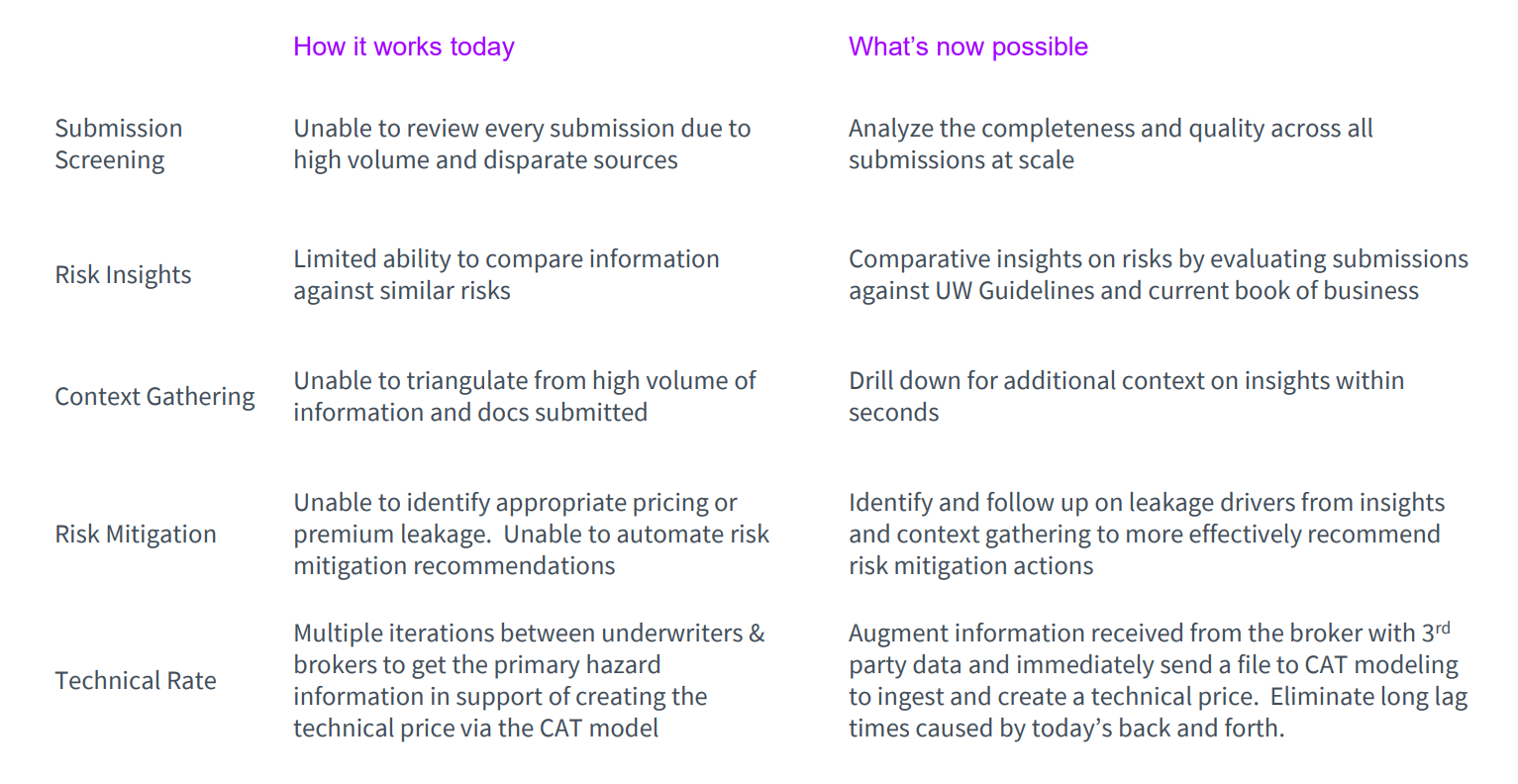

Generative AI allows risk control analysis insights to be highlighted to show loss prevention measures in place as well as the effectiveness of those controls for reducing loss potential. These are critical to informed underwriting decisions and can address areas that are consistently missed or pain points for underwriters in data gathering. Currently when it comes to submission screening, underwriters are unable to review every submission due to high volume and disparate sources. Generative AI allows them to analyze the completeness and quality across all submissions at scale. This means that they move from a limited ability to compare information against similar risks to a scenario where they have comparative insights on risks by evaluating submissions against UW Guidelines and current book of business.

What generative AI can do:

- Generate a comprehensive narrative of the overall risk and its alignment to carriers’ appetite and book

- Flagging, sourcing and identifying missing material data required

- Managing the lineage for the data that has been updated

- Enriching from auxiliary sources TPAs/external data (e.g., publicly listed products/services for insured’s operations)

- Validating submission data against those additional sources (e.g., geospatial data for validation of vegetation management/proximity to building & roof construction materials)

Synthesizing a submission package with third party data in this way allows it to be presented in a meaningful, easy-to-consume way that ultimately aids decision-making. These can all enable faster, improved pricing and risk mitigation recommendations. Augmenting the information received from the broker with third party data also eliminates the long lag times caused by today’s back and forth between underwriters and brokers. This can be happening immediately to every submission concurrently, prioritizing within seconds across the entire portfolio. What an underwriter might do over the course of a week could be done instantaneously and consistently while making informed, structured recommendations. The underwriter will immediately know control gaps based on submission details and where significant deficiencies / gaps may exist that could impact loss potential and technical pricing. Of course, these must then be considered in concert with each insured’s individual risk-taking appetite. These improvements ultimately create the ability to write more risks without excessive premiums; to say yes when you might otherwise have said no.

2) Building & Location details insights aid in risk exposure accuracy

Let’s take the example of a restaurant chain with multiple properties that our insurance carrier is underwriting to illustrate building detail insights. This restaurant chain is in a CAT-prone region such as Tampa, Florida. How could these insights be used to supplement the submission to ensure the underwriter had the full picture to accurately predict the risk exposure associated with this location? The high-risk hazards for Tampa, according to the FEMA’s National Risk Index, are hurricanes, lightning, and tornadoes. In this instance, the insurance carrier had applied a medium risk level to the restaurant due to:

- a past safety inspection failure

- lack of hurricane protection units

- a potential link between a past maintenance failure and a loss event

which all increased the risk.

On the other hand, in preparation for these hazards, the restaurant had implemented several mitigation measures:

- mandatory hurricane training for every employee

- metal storm shutters on every window

- secured outdoor items such as furniture, signage, and other loose items that could become projectiles in high winds

These were all added to the submission indicating that they had the necessary response measures in place to decrease the risk.

Whereas building detail insights expose what is truly being insured, location detail insights show the context in which the building operates. Risk control analysis from building appraisals and safety inspection reports uncover insights showing which locations are the top loss driving locations, whether past losses were a result of covered peril or control deficiency, and adequacy of the control systems in place. In the case of the restaurant chain for example, it did not have its own hurricane protection units but according to the detailed geo-location data, the building is located approximately 3 miles away from the closest fire station. What this really means is that in terms of context gathering, underwriters move from being unable to triangulate from high volume of information and documents submitted to being able to drill down for additional context on insights within seconds. This in turn allows underwriters to identify and follow up on leakage drivers from insights and context gathering to recommend risk mitigation actions more effectively.

3) Operations insights help provide recommendations for additional risk controls

Insured operations details synthesize information from the broker submission, financial statements and information on which aspects are not included in Acord forms / applications by the broker. The hazard grades of each location associated with the insured’s operations and the predominant and secondary SIC codes would also be provided. From this, immediate visibility into loss history and top loss driving locations compared with total exposure will be enabled.

If we take the example of our restaurant chain again, it could be attributed a ‘high’ risk value rather than the aforementioned ‘medium’ due to the fact that the location has potential risks from e.g. catering delivery operations. By analyzing the operation exposure, this is how we identify that high risk in catering :

The maximum occupancy is high at 1000 persons, and it is located in a shopping complex. The number of claims over the last 10 years and the average claim amount could also indicate a higher risk for accidents, property damage, and liability issues. Although some risk controls may have been implemented such as OSHA compliant training, security guards, hurricane and fire drill response trainings every 6 months, there may be further controls needed such as specific risk controls for catering operations and fire safety measures for the outdoor open fire pizza furnace.

This supplementary information is invaluable in calculating the real risk exposure and attributing the correct risk level to the customer’s situation.

Benefits to generative AI beyond more profitable underwriting decisions

As well as aiding in more profitable underwriting decisions, these insights supply additional value as they teach new underwriters (in significantly reduced time) to understand the data / guidelines and risk insights. They improve analytics / rating accuracy by pulling all complete, accurate submission data into CAT Models for each risk and they reduce significant churn between actuary /pricing / underwriting on risk information.

Please see below a recap summary of the potential impact of Gen AI in underwriting:

In our recent AI for everyone perspective, we talk about how generative AI will transform work and reinvent business. These are just 3 ways that insurance underwriters can gain insights from generative AI. Watch this space to see how generative AI will transform the insurance industry as a whole in the coming decade.

If you’d like to discuss in more detail, please reach out to me here.