Other parts of this series:

Technology can help insurers streamline the customer experience—but it also opens the door to new kinds of fraud. Matthew Smith, The Coalition Against Insurance Fraud, on what should be in an insurer’s fraud detection toolkit.

Highlights

- Technology like the Internet of Things, and especially connected home and car, are enabling investigators to recreate a person’s digital path—and in combination with big data, to create a digital mosaic that can fuel insurers’ fraud investigations.

- At the same time, consumer rights to privacy and cyber security are paramount, and insurers must operate within legal and regulatory limits, as well as ethical and moral boundaries.

- An effective anti-fraud plan encompasses all aspects of the insurance company, not just the claims function—and is especially important as insurers strive to provide faster, more seamless customer experiences.

- Insurers must embrace new technologies to protect their company and its policyholders, as well establish the ethics, morals and best practices for how those technologies will be used.

How technology has changed fraud, with Matthew Smith

Matthew Smith is the director of government affairs and general counsel for the Coalition Against Insurance Fraud. He also has nearly three decades of experience in insurance law.

In our previous episode, Matthew talked about the demographics of who commits insurance fraud—and the surprising reasons why they do it. In this episode of the Accenture Insurance Influencers podcast, he shares how technology is helping insurers fight fraud—and how simultaneously, the trend toward frictionless customer experiences is opening the door to new kinds of insurance fraud. Finally, he provides guidance for insurers looking to shore up their fraud detection toolkits.

The following transcript has been edited for length and clarity.

Earlier, we talked about how fraud has shifted over time, and one of the changes was technology and the ability of insurers to use it to better investigate and fight fraud. I understand that you’re a bit of a pioneer in that respect, notably using data from cell phone towers to gather evidence for insurance fraud cases, as well as using social media searches. Why are developments like this important for the fraud detection industry?

They’re extremely important. I think that we’re at the tip of the iceberg right now in terms of where technology is going to lead us over the next decade or probably two decades. As I alluded to earlier, the technology we already have in place today would have been Star Wars technology, even back in the 1980s and early 1990s.

There’s a program I have the privilege of teaching and it’s called, “Where’s Waldo and what’s he up to?” In that program, we’re able to show fraud investigators and people interested in insurance fraud that we all leave a digital path behind us. That path allows an investigator to go in and know exactly where we were and what we were doing yesterday.

We can go back and we can build a model. GPS, loyalty cards, when people stop at a bank and take money out of an ATM, when people go through a toll plaza and use a toll reader, or when people go into their business and scan in with an employee ID, that leaves a digital footprint.

We have the ability to use those digital footprints to go back and verify whether someone’s timeline—of where they say they were, what they say they were doing—matches up with what they are asserting, and the evidence concerning the claim.

Then you couple that with the ability to scrape data or pull data. We can determine who someone communicated with, where they made purchases, when those purchases were made, and put all of that together into a digital mosaic––it allows us to have much more ability to accurately determine where someone was, what they were involved in and whether or not they may have been involved in committing the insurance fraud.

That’s fascinating and also from a personal perspective, slightly daunting to be living at a time when you create that digital footprint just by your everyday moves. And then we’re looking at something like the Internet of Things and connected cars and wearables. How do those play into the conversation?

You know, the Internet of Things is going to truly be fascinating as we see this unfold. But let me give you a real-life example already of where it is becoming reality. Today we have already refrigerators, washers and dryers that have Internet connections. So imagine the ability, when that device in your home is sending constantly data, communicating with other devices on the Internet of Things.

For example, you allege that you were not home yesterday between noon and 4:00 p.m. when the fire occurred. By pulling the data, we can find out that at 2:14 p.m., someone opened and closed the refrigerator door. We can find out that at 3:15 p.m., a load of laundry was started. So all of these pieces that go into the Internet of Things, from Alexa to all of the smart home devices, all create a digital trail.

There have been several fascinating cases. One was a murder case in Arkansas where they were subpoenaing the records of the Alexa device to see what Alexa may have heard leading up to the time of the murder. Now that was a criminal case, not an insurance fraud case, but rest assured those are the cutting-edge cases that are going to take us into the future of what insurance fraud investigators will or will not be able to gain access to.

Wow. And where does consumer privacy fit into all of this?

If you go back to what I said at the start, the Coalition was formed 25 years ago by consumer advocates and insurers. Now we’re in a brave new world as we look at the Internet of Things, as we look at all of the technology that we’ve talked about. But that has to be balanced with protecting consumers’ rights of privacy and cyber security.

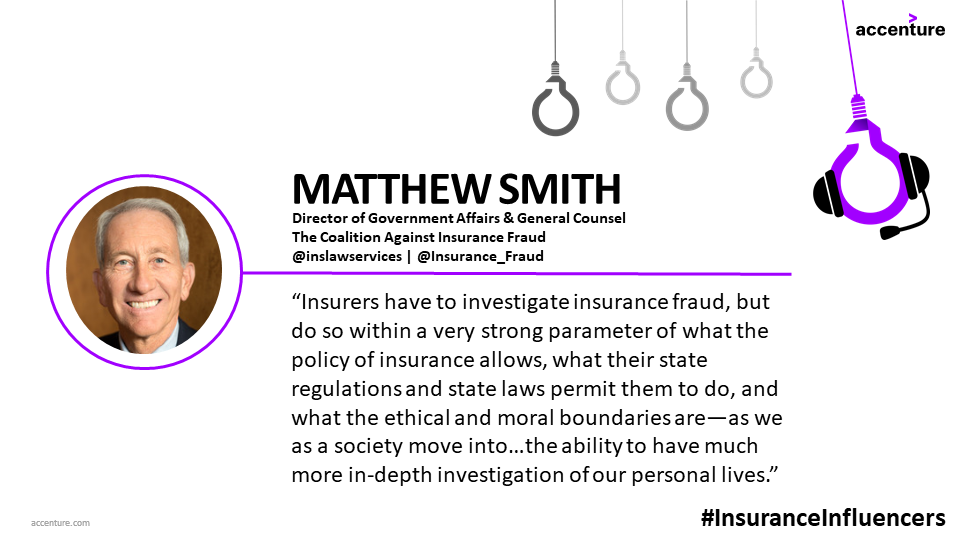

Insurers have to investigate insurance fraud, but do so within a very strong parameter of what the policy of insurance allows, what their state regulations and state laws permit them to do, and what the ethical and moral boundaries are—as we as a society move into this new world of technology, the Internet of Things, and the ability to have much more in-depth investigation of our personal lives.

So one of the true missions now of the Coalition, is to make sure that we and our members are at the forefront of not only recognizing and using these new technologies to fight fraud, but that we are equally the strong voice in leading the call to make sure it is done in best practices––and make certain it is always done with the utmost of ethical and moral protection of the consumer. And we have to keep that at the forefront.

Definitely and an excellent point. Now, I’m curious about the level of technology that we’ve talked about today. Is that typically used by insurers to detect fraud? Or are they using more old-school techniques?

I think we’re in a period of transition and I don’t know that we can quantify and say it’s 60/40, 70/30.

One of the studies that the Coalition does every few years is a technology study as well, and what we are seeing is that more insurers are using technology to identify fraud. They’re starting to use artificial intelligence. They’re using predictive modeling so that they can look at and analyze, not only an insurance claim after it occurs, but also in the underwriting phase to try to prevent insurance fraud from ever occurring. By using those new, emerging technologies for better underwriting practices that do include anti-fraud components.

So I think you are seeing insurers starting, more and more, to integrate these new technologies into their underwriting, their claims and their fraud fighting platforms. But it’s going to be a gradual transition going over the next decade ahead, at least.

Right. And a lot of what we’ve talked about, and I think what a lot of people think about when they think about insurance fraud, is claims fraud. It sounds to me like there’s a push for fraud detection to move earlier into the policy cycle—to point of underwriting or even point of quote.

Absolutely, at all phases. And that’s one of things we do advocate, is that a true anti-fraud plan has to encompass all aspects of any insurance company. You have to look at your agent network, you have to look at internal fraud within the company, you have to look at underwriting fraud. Is that person who is securing that policy a real person or is it an avatar for someone else? Or is it a stolen identity of someone that is being utilized to purchase that policy?

When we get into the claim phase, if it’s a third-party claim, we need to analyze again. Is that the real claimant that was involved in that accident or that incident? Are they fronting for someone else? Do we have reliable and accurate records or have those been falsified? On first-party claims the same factors apply. So it’s all aspects of the insurance process that we look at.

I think we’re at a very curious junction right now, where many insurers are making the shift to become more customer-centric. So we’ve talked about the use of cell phones and there’s this push to make the insurance experience as frictionless as possible, as fast as possible. What does that mean for fraud detection, if especially you’re not dealing with a person face to face?

It’s very interesting because we’re in an era right now where we have better ability than we have had, at any point in history, to investigate insurance fraud. But on the other side of the equation, what you just said is exactly true.

We’re in a world of insurance right now that is becoming so consumer-centric, especially with the dramatic rise of millennials moving into the insurance marketplace, and peer-to-peer insurance, where literally the entire insurance process, from application to underwriting to claims to claims payment, is done on a smart device. We are moving so rapidly to process claims.

If you look at Lemonade, for example, they boast that they have paid a claim in three seconds. And that’s all done with artificial intelligence. Now they will claim they have algorithms built in and programs built in. But as other carriers move toward not using human interaction, but using artificial intelligence and trying to cut down on the processing time of claims, we are going to have new opportunities for fraud.

There’s an ad being run right now by a major insurance company, and it says, “If you can do this…” and it shows a person taking a selfie, “then you can submit your insurance claim.” So we’re inviting people now to no longer have someone go out and inspect a vehicle after it’s been involved in an accident, but just upload pictures of that vehicle. Well, do we know for a fact that’s the vehicle that was involved in the accident?

Or even if it were, here are numerous websites that allow you to alter photos to make it appear as if a perfectly fine vehicle has been involved in a crash. So how we address those emerging trends of insurers wanting to be so fast in taking care of the consumer, and balancing that with the ability that people have to commit high-tech fraud, is going to be very much of a challenge for industry in the emerging years.

Those sound like some big issues arising from what is probably a need to update the insurance industry and its processes. So as insurers look to shore up their fraud detection toolkits—and we’ve talked about so many different things that they have at their disposal today—what should they be focusing on in order to set themselves up for success for the next 5 to 10 years? What needs to be in that toolkit?

The number one thing they need in their toolkit is to embrace the new technologies that are out there to protect not only the company, but more importantly to protect the company’s policyholders who put their trust in the company. But equally in that toolbox, you’ve got to put in there ethics, morals, best practices, and written policies and procedures on how these new technologies are going to be used. Things like: who has access to this data, how will the data be used, how do we share it with policyholders, what data we are going to require them to present to us in the event that they make a claim? So that everything is disclosed upfront very fairly, very honestly and we know the parameters of how we’re going to use these new technologies.

When we talk with our carrier members, we talk to insurers about the need to embrace the new technologies that are there. Use them to protect your policyholders and your company, but make certain at the forefront of everything you do, you are leading with strong moral and ethical guidelines—and communicating to your policyholders what you’re doing and how you’re going to be using this new data that is emerging, and that we are gathering and using to fight insurance fraud.

Matthew, thank you so much for taking the time to speak to us today.

Thank you. It’s been my privilege, my honor to be a part of the podcast.

Summary

In this episode of the Accenture Insurance Influencers podcast, we talked about:

- The digital path that people leave in today’s connected world. In combination with data, it can enable investigators to create a digital mosaic to better detect fraud.

- Advancing technology and data must be used responsibly, with consumer privacy, data ethics and cyber security at their core.

- Anti-fraud efforts go far beyond the point of claim; they should encompass all aspects of the insurance company.

- As insurers prepare for a digitally driven future, they must embrace new technologies to advance their fraud detection capabilities—and incorporate ethics, morals and best practices to be transparent about how those technologies will be used.

For more guidance on a digitally driven future of fraud detection:

- Check out Accenture Technology Vision for Insurance 2019.

- Learn ten steps to improving data transparency.

- Read about the state of cyber resilience in insurance.

That wraps up our conversation with Matthew Smith. In two weeks, we’ll speak with Eric Joost from Willis Towers Watson about the evolving role of the broker, and why customer-centricity and risk management go hand in hand. Until then, you can catch up with previous episodes of the Accenture Insurance Influencers podcast. We spoke to Ryan Stein about how self-driving cars are challenging today’s insurance rules and Lex Sokolin about how artificial intelligence could change insurance.

What to do next:

- Visit com/insuranceinfluencers for more information or subscribe directly here:

Contact us if you’d like to be a guest on the Insurance Influencers podcast.