Other parts of this series:

In Europe and across the world, there’s hope that life will start to return to normal this year. But although people may begin to work, socialise and travel as we used to, the way we purchase insurance – and indeed what we want from our insurers – will never be the same.

How can we be sure? Because we asked people. In summer 2020, Accenture surveyed 23,400 European consumers in 15 countries – part of a global survey of over 47,000 consumers. Many of the behaviour shifts we noted then have accelerated as restrictions have persisted.

The survey results are striking. They show COVID-19 triggered a sudden shift in consumer expectations and demands of insurers that might otherwise have taken decades to materialise. Four of these findings are particularly noteworthy.

1. Digital engagement surges

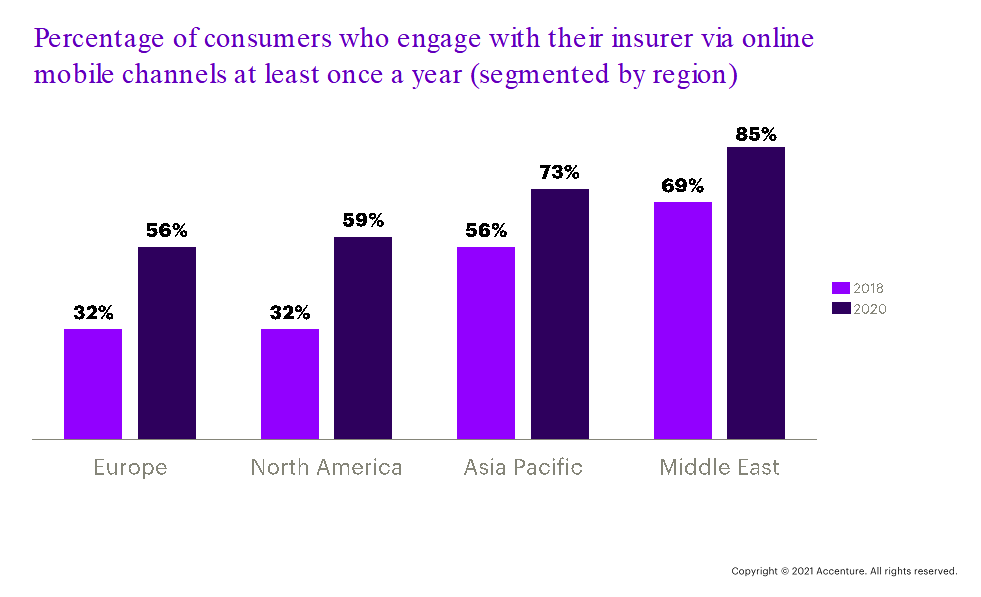

European consumers’ use of digital channels to engage with their insurer rocketed in the last two years (though it’s still lower than peers elsewhere, as the diagram shows): 56 percent interact with their insurer via online mobile channels at least once a year, compared with just 32 percent in 2018.

Just over a quarter of European consumers (26 percent) engage with their insurer this way at least once a month, compared with only 11 percent in 2018.

Despite that rapid increase, Europe lags the world on digital usage. Indeed, 39 percent of North American consumers engage their insurer via mobile channels at least once a month, as do 45 percent of consumers in Asia-Pacific, 54 percent in Brazil and 56 percent in the Middle East. The figures for consumers who used these channels at least once a year, as the diagram shows, are higher.

This raises a key question. Is the spike in digital uptake a short-term aberration caused by the unique circumstances of lockdowns? After all, the survey was conducted when consumers were confined to their homes to varying degrees, and were experimenting with digital channels for everyday purposes.

We think not. While some consumers may revert to more traditional methods of engagement, the majority will persist with the digital behaviour they have become accustomed to in recent months. And why wouldn’t they? After all, two-thirds of European consumers say they’re satisfied with online mobile channels, while just 5 percent are dissatisfied.

2. Value for money rises up the agenda

Value for money is today the most important factor for consumers when dealing with banks and insurers; in 2018, it was in fifth place. The parlous economic climate explains why customers have become more cost-conscious, but this doesn’t mean price alone holds the solution to retaining existing business and winning over new policyholders.

By offering solutions that are simple, convenient and, importantly, tailored to each user’s personal circumstances, insurers can create a good impression. Indeed, an ability to manage accounts in a way that suits the customer is the second-most important factor that consumers cite when dealing with financial services companies.

Many insurers, of course, already do this. The key is to marry these services with competitive pricing.

Insurance Revenue Landscape 2025: Our report examines 4 key areas of innovation that offer revenue opportunities for insurers over the next 5 years..

Learn more3. Personalisation is pivotal

European consumers’ appetite for personalised services soared during the pandemic. Take automotive insurance: 76 percent expressed an interest in automotive insurance that ties premiums to safe driving, compared with 54 percent two years earlier. In addition, 70 percent of Europeans are interested in pay-as-you-drive automotive insurance; that’s up from 52 percent.

We also found that more European consumers want personalised life insurance – 58 percent are interested in life insurance where premiums are tied to a healthy lifestyle, up from 40 percent in 2018.

This clamour for personalised insurance is partly a result of a desire for lower prices. However, consumers might well feel, too, that altering their driving behaviour and adopting a healthier lifestyle should offer a route to lower premiums. It also reflects the fact that COVID-19 encouraged many people to drive less and to lead healthier lifestyles – and they want their insurance to reflect this.

4. Protecting home digital infrastructure is paramount

With lockdowns forcing entire populations to work, socialise and shop from home, European consumers have become extremely reliant on the IT infrastructure – which for most is a computer, Wi-Fi and online accounts – that enables this.

That’s caused many to think for the first time about protecting their residential digital infrastructure. Importantly, they’re prepared to take advice on this from their insurer: 74 percent of European consumers would be interested in assistance dealing with cybersecurity threats if offered by their bank or insurer, while 45 percent are interested in cybersecurity insurance for their home where premiums are tied to using the latest virus protection software.

Some insurers have already started to offer this type of assistance, and our survey shows this will be well received. It’s also unlikely that consumers will become more relaxed about protecting their digital infrastructure when the pandemic recedes – after all, 51 percent of those that can work from home intend to do so more frequently after COVID-19.

In other words, our survey shows consumers have adapted extremely quickly to these unprecedented circumstances. To meet their new expectations, insurers will also have to move fast.