Other parts of this series:

Process efficiencies are just the start

As I have noted in earlier posts in this series, insurance organizations have experimented with blockchain and distributed ledger technology (DLT) for several years. They initially conducted their proofs of concept and pilots on public, permissionless technologies such as Ethereum. Despite the industry hype, most of these early experiments did not deliver the value that organizations expected. Companies were also unsure how to take them into production.

Investment has since shifted from these public networks to private, permissioned DLT networks like Corda and Hyperledger Fabric. At this stage of evolution, these types of platforms are proving to be the best fit with evolving enterprise DLT requirements around data, security, and risk, especially as DLT networks move to live production.

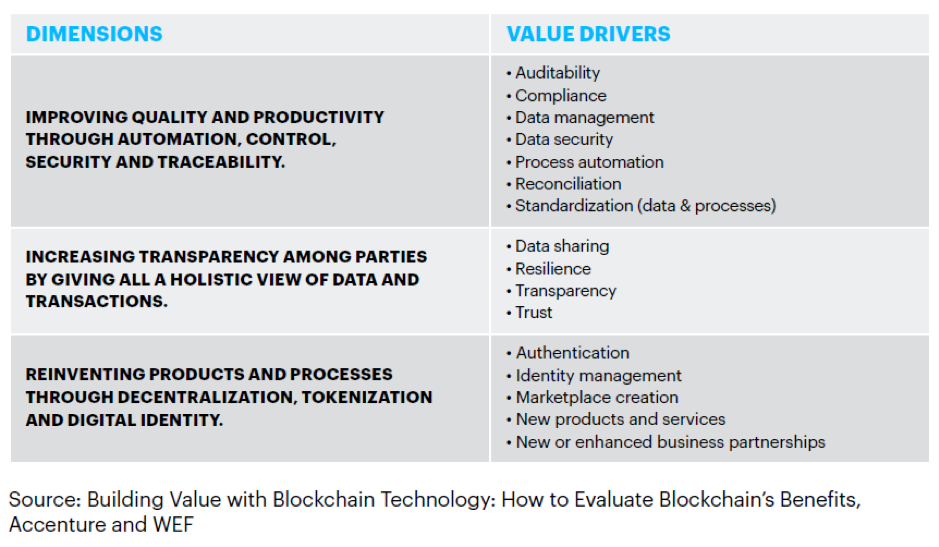

Such technologies are also better suited to new, emerging models of collaboration, with insurance organizations seeing the real value of DLT in its ability to enable different parties to share a unified view of the core information that drives an ecosystem. Providing a single source of truth allows friction in business processes to be drastically reduced, using solutions such as smart contracts to facilitate and automate DLT networks.

More efficient processes: just the start

Data reconciliation is made easier, accuracy is improved, and time spent uncovering information is eliminated, allowing for transparency, efficiency gains and cost reductions throughout a value chain. What’s more, shared industry tasks and automation generate more seamless processes and lower total cycle time.

The aggregate improvements in speed and accuracy can also create a more positive customer experience. For example, shortening the claims cycle through improved efficiency could lead to higher customer satisfaction and retention, while faster and better access to data could enable smoother interaction between insurers and their customers. Reducing inefficiencies and costs throughout the value chain could, ultimately, even lead to lower premiums.

A tool to identify the value of DLT

But these tangible improvements over today’s process inefficiencies will only be the beginning.

As insurers become accustomed to a new way of working and product vendors deliver more robust production-grade solutions, we will see a second wave of growth that enables new products and service models. DLT will drive data quality to new levels of consistency and reliability, allowing more effective integration of solutions such as artificial intelligence, real-time analytics, and the Internet of Things into insurers’ business models.

We are still early in the adoption cycle for this wave of technologies, but some insurance organizations are already starting to lay the groundwork for innovation across their value chains and marketplaces. Consortiums, where groups of organizations commit resources towards a common cause, appear to be successful drivers in this early phase of DLT adoption.

By coming together, companies in these consortiums are able to combine their experience and resources to overcome the hurdles to DLT adoption. In establishing business networks that capture efficiency gains, these first-movers are laying the foundation of future transformational and disruptive impact for the entire industry.

My final post in this series will look at two possible models insurance organizations can follow for collaborating with other members of their ecosystem to put DLT platforms in place. In the meantime, check out our report, The blockchain breakthrough in insurance to learn more.